How Payment Fraud Hides in Your Systems: The AP Vulnerabilities CFOs Must Surface

Picture this

It's 4:47 PM on a Friday when your AP manager receives an urgent email from your largest supplier. "Due to a banking merger, we need to update our payment details immediately to avoid disruption to your supply chain." The attached bank change form looks identical to previous ones—same letterhead, same authorized signature, same routing format. Your team processes the change through your standard verification workflow, and Monday's $340,000 payment goes out seamlessly.

Two weeks later, your supplier calls asking why their invoice remains unpaid. That's when you discover the bitter truth: sophisticated fraudsters had studied your supplier relationship for months, created pixel-perfect documentation, and exploited a vulnerability hiding in plain sight within your ERP system's vendor master file process.

This isn't a story about security breaches or phishing emails. This is about the most dangerous type of B2B fraud: the kind that weaponizes your own AP systems against you.

The Systems Fraudsters Target Most

Every CFO today relies on interconnected systems that drive AP efficiency—but these same systems create hidden vulnerabilities that sophisticated fraudsters systematically exploit:

- ERP Platforms (SAP, Oracle, NetSuite): With 95% of more than 600 SAP systems tested vulnerable to attack, primarily due to unapplied patches, these core business systems present significant fraud opportunities.

- Invoice Processing Systems (Basware, Coupa, Concur): Document authenticity gaps that struggle to detect AI-generated forgeries, with 40% of BEC emails now AI-generated according to VIPRE's 2024 Email Threat Trends Report.

- Payment Automation Tools (Bank of America CashPro): API vulnerabilities and automated execution risks that enable rapid fraud execution.

- Vendor Management Portals: Identity verification weaknesses that enable false supplier creation.

- Banking Integration Systems: Real-time processing capabilities that execute fraudulent transactions at business speed.

The latest 2025 AFP Payments Fraud and Control Survey reveals that 79% of organizations experienced actual or attempted payments fraud in 2024, with Business Email Compromise remaining the dominant attack vector at 63% of incidents. Critically, 62% of payment fraud originated from fraudulent emails, demonstrating how external attackers exploit internal systems without requiring direct access.

The data shows a clear pattern: the vast majority of payment fraud originates externally, with only 3% attributed to internal actors according to the AFP survey, while Business Email Compromise (62%) and external individual actors (49%) represent the primary external threats. This means fraudsters are succeeding by understanding and manipulating your systems from the outside, not by breaching your security perimeters.

As the AFP survey notes, "Fraudsters are using AI and are able to target messages very effectively, hindering the ability of employees to differentiate a fraudulent email from an authentic one."

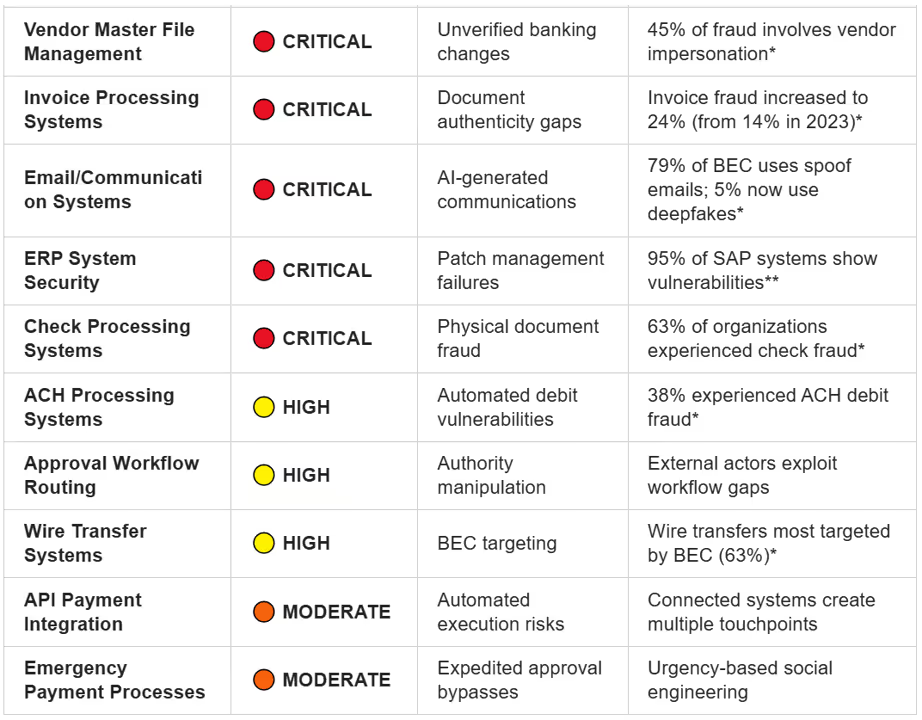

Infrastructure Vulnerability Assessment: Where Fraud Hides

To effectively protect your organization, you must first understand where vulnerabilities exist within your payment infrastructure. The matrix below reveals the hidden risk levels across critical AP components, updated with 2025 fraud intelligence:

AP Infrastructure Risk Assessment Matrix

*Source: 2025 AFP Payments Fraud and Control Survey, Truist Summary Report

**Source: Eftsure ERP Statistics

Critical Risk Indicators by Component

🔴 CRITICAL RISK - Immediate Action Required

- Email Systems: 62% of all fraud originates from fraudulent emails, with AI making detection increasingly difficult

- Vendor Master Files: 45% of fraud involves vendor impersonation attacks

- Invoice Processing: Invoice fraud jumped 71% year-over-year (14% to 24%)

- Check Systems: Despite digitization, 63% of organizations still experience check fraud

🟡 HIGH RISK - Enhanced Controls Needed

- ACH Systems: 38% of organizations experienced ACH debit fraud, up from 33% in 2023

- Wire Transfers: Most targeted payment method for BEC attacks

- Approval Workflows: External actors increasingly exploit emergency overrides and authority confusion

🟠 MODERATE RISK - Monitoring Required

- Deepfake Technology: While deepfake attempts affected only 5% of organizations in 2024, FinCEN reported an increase in suspicious activity reports describing suspected deepfake use beginning in 2023 and continuing through 2024

The Emerging AI Threat: Beyond Traditional Fraud

AI is now being used to create "higher quality and therefore more effective fraudulent emails" that are increasingly difficult to distinguish from legitimate communications.

AI-Enhanced Attack Vectors

- Document Generation: AI creates pixel-perfect invoice replicas and banking forms that bypass traditional verification methods.

- Communication Sophistication: Machine learning enables fraudsters to mimic organizational communication patterns, timing, and language with unprecedented accuracy.

- Behavioral Mimicry: AI analyzes publicly available information to create convincing impersonations of vendors, executives, and business partners.

- Adaptive Response: Fraudsters use AI to monitor defensive measures and adjust tactics in real-time.

The AFP warns: "Advances in AI will enable scammers to produce videos and images to easily deceive targets," with FinCEN issuing alerts about increasing deepfake fraud schemes in late 2024.

The CFO's System Audit: Exposing Hidden Vulnerabilities

Traditional fraud prevention focuses on detecting obvious red flags, but the 2025 data shows that the vast majority of fraud originates externally through system exploitation rather than security breaches. CFOs must examine operational blind spots that fraudsters systematically target.

Priority Assessment Areas Based on 2025 Threat Intelligence

Email and Communication Security

- How does your organization verify the authenticity of supplier communications?

- What AI-powered detection capabilities exist for identifying generated content?

- Are external emails clearly flagged and subject to enhanced scrutiny?

Vendor Master File Integrity

- What verification processes protect against the 45% of fraud attempts involving vendor impersonation?

- How quickly can unauthorized changes be detected and reversed?

- Are banking detail modifications subject to callback verification?

Invoice Processing Controls

- Can your systems detect the increasingly sophisticated AI-generated invoices?

- What cross-referencing occurs with historical vendor patterns and external data sources?

- How do you verify invoice authenticity beyond basic format checking?

Check and ACH Security

- Given that 63% of organizations experience check fraud, what physical and digital controls protect your check processes?

- How do you monitor the 38% increase in ACH debit fraud targeting?

- What real-time alerts exist for unusual payment patterns?

The Modern Control Framework Gap

Data reveals that while 94% of organizations have policies for verifying vendor changes, and 96% provide fraud training, these traditional controls aren't keeping pace with AI-enhanced threats. Organizations need dynamic, intelligence-driven approaches that can adapt to evolving fraud sophistication.

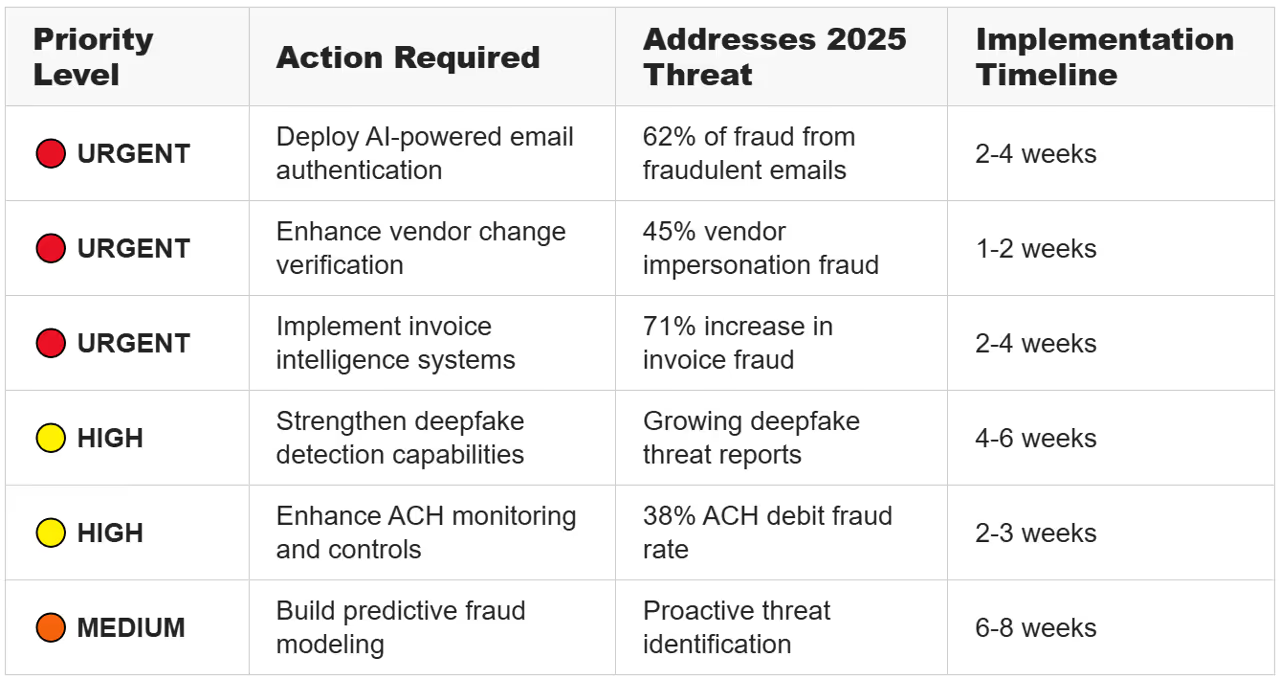

Strategic Response Framework: Beyond Traditional Controls

Based on the 2025 threat landscape, CFOs must implement multi-layered defenses that address both current and emerging fraud vectors:

Immediate Action Priorities Matrix

Implementation Checklist by Threat Vector

Email-Based Fraud Defense (62% of all fraud)

- Deploy AI-powered email authentication and content analysis

- Implement enhanced external email flagging and verification

- Establish callback verification for all payment-related communications

- Create deepfake detection capabilities for voice and video communications

Vendor Impersonation Protection (45% of fraud attempts)

- Enhanced vendor master file monitoring and change detection

- Multi-channel verification for banking detail modifications

- Real-time behavioral analysis of vendor communications

- Integration with external vendor verification databases

Invoice Fraud Prevention (24% of incidents, 71% increase)

- AI-powered document authenticity verification

- Cross-reference systems for historical invoice patterns

- Enhanced approval workflows for new or modified invoices

- Real-time integration with supplier databases

Payment Method Security

- Enhanced check fraud controls (93% positive pay implementation recommended)

- ACH debit blocking and filtering (92% of organizations block except designated accounts)

- Wire transfer verification protocols (callback verification for 91% of organizations)

- Multi-factor authentication for all payment systems (92% implementation rate)

The Financial Impact Reality

The 2025 AFP data provides crucial context for CFO decision-making around fraud prevention investments:

- Loss Distribution: While 46% of organizations avoided financial losses, 54% experienced actual losses, with 21% losing under $25,000 and 18% losing more than $50,000.

- Recovery Challenges: Only 22% of organizations recovered more than 75% of fraud losses, down dramatically from 41% in 2023. This declining recovery rate makes prevention increasingly critical.

- Hidden Costs: Beyond direct losses, organizations face business continuity disruption, regulatory compliance risks, and damaged stakeholder relationships.

The data shows that while individual fraud incidents may seem manageable, the combination of increasing frequency, declining recovery rates, and business disruption costs creates substantial organizational impact.

Competitive Advantage Through Advanced Fraud Prevention

Organizations implementing comprehensive, AI-powered fraud prevention capabilities position themselves for multiple strategic advantages:

- Operational Excellence: The 96% of organizations with comprehensive fraud training and the 94% with strong verification policies demonstrate measurably better fraud outcomes.

- Supplier Trust: Robust security measures build confidence with vendors, enabling stronger partnership relationships and potentially better payment terms.

- Market Positioning: Advanced fraud prevention capabilities support entry into new markets and business relationships that require demonstrated security sophistication.

- Regulatory Confidence: Strong fraud controls support compliance with evolving regulatory requirements and reduce audit risk.

- Cost Management: Proactive fraud prevention delivers measurable ROI compared to reactive incident response and recovery efforts.

Your Strategic Fraud Prevention Transformation

The data makes clear that traditional, reactive approaches to fraud prevention are inadequate against AI-enhanced threats. CFOs must lead a transformation toward predictive, intelligence-driven fraud prevention that treats security as a competitive capability.

The fraudsters are already using AI to study your systems, generate convincing communications, and exploit your processes with increasing sophistication. The growing deepfake threat and the 71% jump in invoice fraud (to 24% in 2024 from 14% in 2023) demonstrate that this threat is accelerating rapidly.

The question isn't whether AI-enhanced fraud will target your organization—the AFP data shows it's already happening. The question is whether you'll build the predictive capabilities necessary to stay ahead of this evolving threat while transforming fraud prevention from a cost center into a strategic advantage.

Ready to transform your AP systems from fraud targets into competitive advantages? The technologies and strategic frameworks exist today to make this transformation possible.

The future of finance is AI-protected, intelligence-driven, and strategically valuable. Make sure your organization is ready.

Learn how Finexio's AI-powered AP Payments as a Service platform helps CFOs build fraud-resistant operations that deliver measurable ROI while enhancing operational efficiency. Our embedded intelligence approach addresses the specific fraud vectors identified in the 2025 AFP survey, transforming your payment infrastructure from vulnerability to competitive advantage.

Ready to get started? Contact Finexio to schedule a strategic consultation on transforming your fraud prevention capabilities based on the latest threat intelligence.

Sources:

Association for Financial Professionals. "2025 AFP Payments Fraud and Control Survey Report." Association for Financial Professionals, 2025. Truist Summary Report. https://www.truist.com/content/dam/truist-bank/us/en/documents/info/cci/2025-afp-payments-fraud-control-survey-report-key-highlights.pdf

Eftsure. "ERP Statistics 2025." Eftsure, 2025. https://www.eftsure.com/statistics/erp-statistics/

VIPRE. "Email Threat Trends Report Q2 2024." VIPRE Security, 2024. https://vipre.com/wp-content/uploads/2024/07/vipre-q2-2024-email-threat-report.pdf

Get the free Newsletter

Get the latest information on all things related to B2B and electronic payments delivered straight to your inbox.