Payments as a Service vs AP Automation: Key Differences

Your AP team approved the invoice three days ago. It’s sitting in a queue. Someone still needs to print a check, stuff an envelope, and drop it in the mail. Or maybe they need to log into a banking portal, key in ACH details, and hope the routing number is right.

This is the gap nobody talks about. The invoice is approved. The payment hasn’t moved.

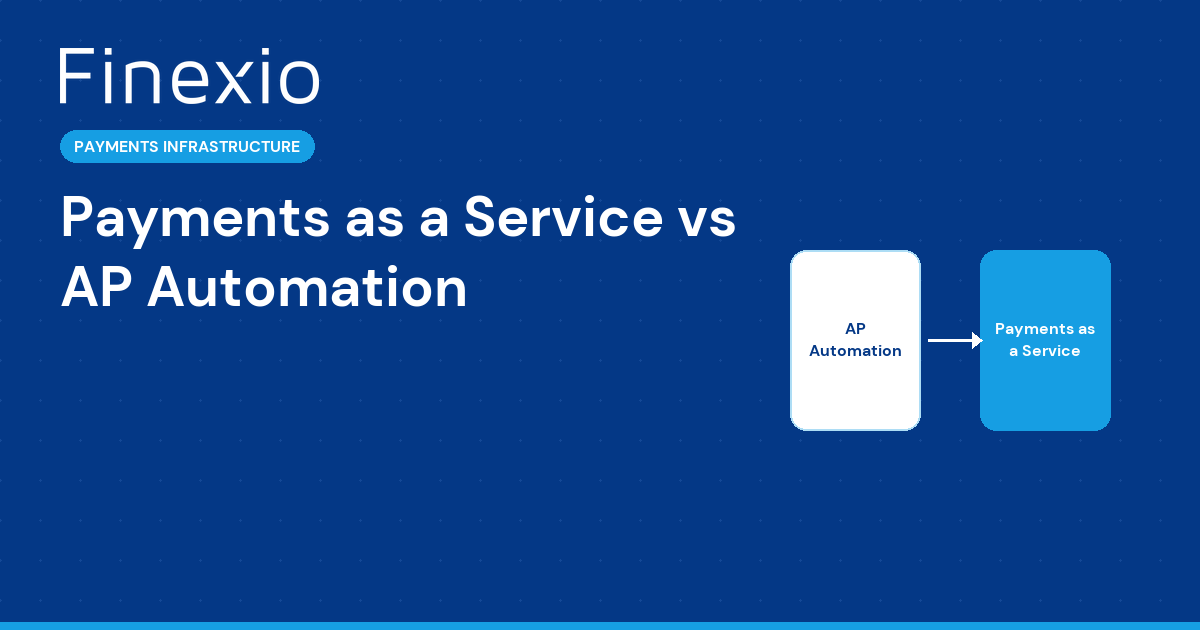

AP automation platforms have done an impressive job solving the front half of accounts payable. Invoice capture, coding, routing for approval. That workflow is well understood, and dozens of vendors compete to make it faster. But once an invoice is approved, most organizations drop back into manual processes to actually move the money. That is exactly where Payments as a Service comes in.

What AP Automation Actually Does

AP automation covers the intake-to-approval workflow. Think of it as everything that happens before someone says "yes, pay this."

That includes scanning or ingesting invoices, matching them against purchase orders, coding to the right GL accounts, and routing them through approval chains. Good AP automation saves hours of data entry and reduces errors in the matching process.

But here is the thing most buyers miss when evaluating these platforms. AP automation does not make payments. It does not connect to banking infrastructure. It does not manage supplier payment preferences. It does not handle fraud screening, compliance checks, or payment delivery across multiple rails.

Once the invoice clears approval, AP automation hands off to... whatever your team has cobbled together.

What Payments as a Service Covers

Payments as a Service picks up exactly where AP automation stops. It handles the full payment lifecycle after approval. One file goes in. Every payment gets delivered, whether that payment moves by virtual card, ACH, or check.

Finexio pioneered this category with more than 10 years in market and over $75 million in investment. The Finexio platform sits on J.P. Morgan Chase banking infrastructure, with Mastercard and Visa partnerships backing the card programs.

Here is what that means in practice. After your AP system approves an invoice, Finexio receives one payment file. From there, the platform determines the best payment method for each supplier, screens for fraud, validates bank accounts, and executes the payment. Your AP team does not touch the payment again.

The Gap Between Approval and Payment

Industry data shows the average manual B2B payment costs $8.93 to process. That number includes the labor, materials, banking fees, and error correction involved in getting money from your account to a supplier’s account.

Most organizations have invested in AP automation and still carry that $8.93 cost per payment. Why? Because they automated invoices but not payments.

Think about what happens after approval in a typical organization. Someone downloads a payment file. They log into one or more banking portals. They key in payment details or upload batch files. They print and mail checks for suppliers who don’t accept electronic payments. They field calls from suppliers asking where their money is.

That is all manual work that AP automation was never designed to handle.

Why This Matters for Your Bottom Line

The financial impact goes beyond labor costs. Manual payment processes are where fraud lives. AFP research shows that 80% of payment fraud targets manual processes. Every time a human touches payment data, keys in account numbers, or handles a paper check, the attack surface grows.

Finexio addresses this directly. The platform runs bank account validation, KYC/AML screening, and OFAC sanctions checks on every payment. Finexio Shield backs it with a $1$2 million fraud guarantee, which is something no AP automation platform offers because they are not in the payment execution business.

How They Work Together

This is not an either/or decision. AP automation and Payments as a Service are complementary. The best accounts payable operations use both.

Your AP automation platform handles invoice intake through approval. Finexio handles everything after approval. The handoff is a single payment file. No manual intervention. No portal hopping. No check printing.

Finexio integrates with the major AP automation and ERP platforms specifically to make this handoff clean. The result is a fully automated procure-to-pay process where invoices flow in, get approved, and payments go out without your team touching the payment itself.

What to Look for in a Payments as a Service Provider

Not every payment platform qualifies as true Payments as a Service. Here is what separates a real platform from a bolt-on feature.

Banking infrastructure matters. Finexio is built on J.P. Morgan Chase, the largest bank in the United States. That is not a partnership logo on a slide deck. That is the actual banking rail your payments move through.

Multi-rail execution is required. A real Payments as a Service provider handles virtual cards, ACH, and checks from a single file. If you still need to manage separate processes for different payment types, you do not have Payments as a Service.

Supplier enablement is the engine. The provider should be actively converting your suppliers to accept virtual cards, which generates rebate revenue for your organization. Finexio treats supplier enablement as a core competency, not an afterthought.

Frequently Asked Questions

Can I use Payments as a Service without AP automation?

Yes. Finexio works with or without an AP automation platform. If your team approves invoices in an ERP like SAP, Oracle, or NetSuite, Finexio can accept a payment file directly from that system. AP automation makes the front half faster, but it is not a prerequisite for automating payments.

Does Payments as a Service replace my bank?

No. Finexio is not a bank. Finexio orchestrates payments using J.P. Morgan Chase banking infrastructure. Your existing banking relationships stay in place. Finexio handles the complexity of routing payments across multiple methods so your team does not have to.

How fast can we go live with Payments as a Service?

Most Finexio implementations are measured in weeks, not months. The integration is a single payment file from your existing system. There is no rip-and-replace of your AP workflow. You keep your current approval process and add payment execution on top.

Ready to close the gap between invoice approval and payment delivery? Finexio handles the full payment lifecycle so your AP team can stop processing payments and start focusing on strategy. Book a Consultation to see how Payments as a Service fits your current AP workflow.

Get the free Newsletter

Get the latest information on all things related to B2B and electronic payments delivered straight to your inbox.