The Three-Party Model: How B2B Payment Infrastructure Works

Most businesses think of payments as a two-party transaction. You owe a vendor. You pay the vendor. Done.

This mental model made sense when payments meant writing a check. But modern B2B payment infrastructure involves three distinct parties with three distinct roles. Understanding this separation explains why some organizations struggle with payments and others have solved the problem entirely.

The three-party model is not a product pitch. It is a framework for understanding how money actually moves in B2B commerce today.

The Old Model: Two Parties and a Check

For decades, the AP team approved an invoice, printed a check, and mailed it. Simple. Also slow, expensive, and insecure. The average cost of processing a single manual B2B payment is $8.93. That does not include fraud, payment errors, or the supplier relationship damage from slow payment cycles.

AP automation platforms emerged to digitize the approval process. But a gap remained between approval and payment delivery. Approving an invoice faster does not mean the payment arrives faster. That gap is where the three-party model comes in.

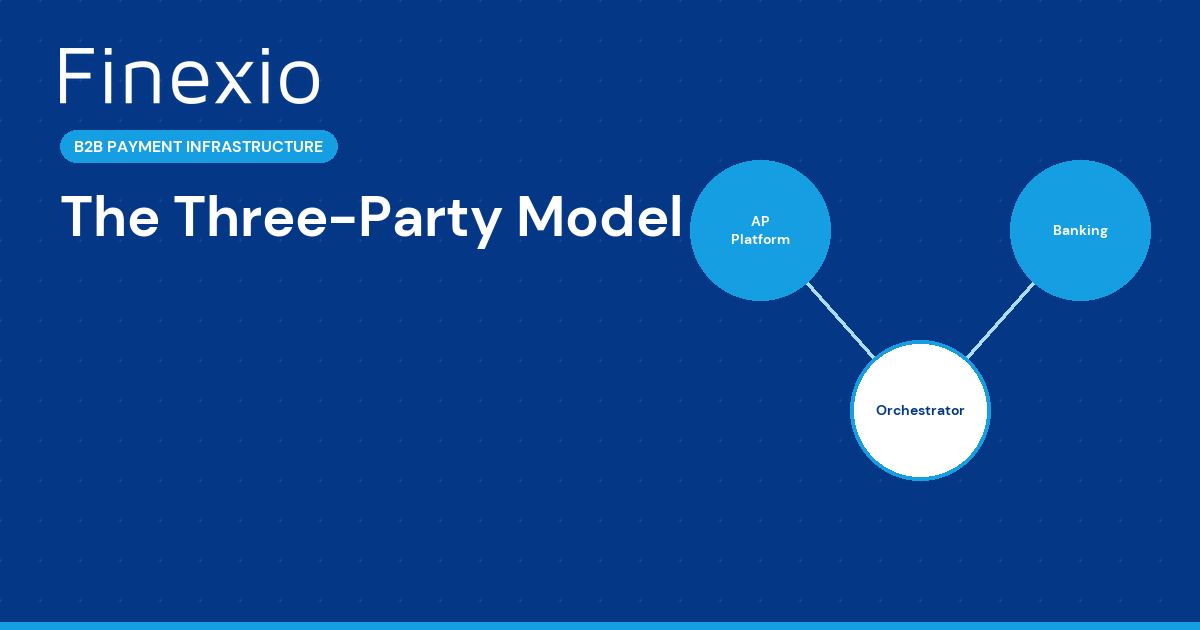

The Three Parties, Defined

Modern B2B payment infrastructure separates into three layers, each with a specific function.

Party 1: The AP Platform or ERP

This is where invoices are captured, coded, routed for approval, and authorized for payment. Whether it is an ERP like SAP or Oracle, an AP automation platform, or a vertical-specific solution, this layer owns the business logic: who gets paid, how much, and when.

The AP platform is where your team does its work. It handles the "should we pay this?" question.

It does not handle the "how do we deliver this payment?" question. And that distinction matters.

Party 2: The Payment Orchestrator

This is the layer between approval and banking. The payment orchestrator takes the approved payment file and handles everything required to deliver funds to the right supplier through the right payment rail at the right time.

This includes supplier management (knowing which vendors accept virtual cards, ACH, or checks), payment routing (selecting the optimal rail for each transaction), banking validation (verifying that payment destinations are legitimate), fraud screening (OFAC checks, real-time monitoring), exception handling (managing failed payments, returned ACH, expired cards), and reconciliation (confirming delivery and reporting back).

Finexio operates in this layer. As an AP Payments as a Service platform, Finexio takes a single payment file from the AP platform and orchestrates every payment through to delivery. One file in. Every payment delivered.

Party 3: The Banking Infrastructure

This is where money actually moves. Banks process ACH transactions through the Federal Reserve's ACH network. Card networks (Mastercard, Visa) process virtual card transactions. The banking layer is regulated, audited, and built for the secure movement of funds.

Finexio is built on J.P. Morgan Chase banking infrastructure. J.P. Morgan Chase is the issuing bank. This means payments processed through Finexio move through one of the world's largest and most regulated financial institutions.

Finexio is not a bank. This is an important distinction. The three-party model works because each party specializes in what it does best.

Why Separation of Concerns Matters

Each component does one thing well. The system is stronger because no single layer is overloaded with responsibilities.

Your AP platform should focus on approvals. Coding invoices, routing them for approval, managing payment terms. That is complex enough. Asking the same platform to also manage banking relationships, supplier enrollment, and fraud detection creates a system that does many things poorly instead of one thing well.

The payment orchestrator should focus on delivery. Finexio does not approve invoices. It takes the approved file and handles the operational complexity of getting money from point A to point B across multiple payment rails and thousands of suppliers.

The bank should focus on moving money. J.P. Morgan Chase processes transactions through regulated banking infrastructure. It does not manage your supplier relationships or route your payments.

When these three layers are combined into a single system (or handled manually), the result is the $8.93-per-payment reality that most organizations still live with.

More Secure, More Efficient, More Cost-Effective

Security improves when duties are separated. No single party has end-to-end control. Your AP team authorizes payments but does not execute them. Finexio executes payments but does not authorize them. J.P. Morgan Chase moves funds but does not determine recipients. A fraudster who compromises one layer cannot redirect payments without also compromising another. Finexio adds bank account validation, OFAC screening, real-time monitoring, and the Finexio Shield $2M fraud guarantee on top of this structural protection.

Specialization drives efficiency. When an AP platform tries to also be a payment processor, the result is limited payment rails, minimal supplier enablement, and basic fraud controls. A dedicated orchestrator like Finexio invests entirely in the payment delivery problem. That means support for every payment rail, supplier enablement teams that achieve enrollment targets in under 90 days, and fraud prevention backed by more than $75M in platform investment. Platform partners who embed Finexio's infrastructure can also monetize the payments flowing through their systems.

The economics favor buy over build. Building payment infrastructure in-house means maintaining banking relationships, managing PCI DSS compliance, staffing supplier enablement, and investing in fraud detection. For most organizations, this is overhead, not a core competency. The three-party model lets each party invest in what it does best. Lower cost per payment. Faster delivery. Stronger fraud prevention.

The Bottom Line

The two-party model of B2B payments, where the payer and payee handle everything, is a legacy of the paper check era. Modern B2B payment infrastructure separates authorization, orchestration, and banking into three specialized layers.

This is not theoretical. It is how Finexio processes payments today for organizations across healthcare, construction, higher education, hospitality, and manufacturing. One file drops from the AP platform. Finexio orchestrates the payment. J.P. Morgan Chase moves the money.

Three parties. Three specialties. One payment delivered.

Frequently Asked Questions

What is the difference between an AP automation platform and a payment orchestrator?

An AP automation platform handles invoice capture, coding, approval routing, and payment authorization. It answers the question of who gets paid, how much, and when. A payment orchestrator like Finexio takes the approved payment file and handles everything after that: routing the payment through the right rail, managing supplier enrollment, validating banking information, screening for fraud, handling exceptions, and confirming delivery. They are complementary layers, not competing ones.

Why does Finexio use J.P. Morgan Chase as its banking infrastructure?

J.P. Morgan Chase is one of the world's largest and most regulated financial institutions. By building on J.P. Morgan Chase infrastructure with Mastercard and Visa partnerships, Finexio provides banking-grade security and reliability without requiring each client to establish and maintain their own banking relationships for payment processing. This is the specialization principle of the three-party model in action.

Can my current AP platform work with this three-party model?

Yes. Finexio integrates with AP automation platforms, ERPs, and vertical-specific software through its platform connections. Your team continues using the AP system they already know for approvals. Finexio receives the approved payment file and handles delivery. No changes to your approval workflow are required.

Want to see how the three-party model works for your organization? Book a Consultation with Finexio.

Get the free Newsletter

Get the latest information on all things related to B2B and electronic payments delivered straight to your inbox.